Feeling Your Net Worth Is Too Short? Here's How To Grow It In 2024

Do you ever get that sinking feeling, a quiet worry that your financial standing, your personal net worth, just isn't quite where it ought to be? It's a rather common thought, particularly these days, when so many folks are grappling with rising costs and uncertain futures. That sensation of having a "too short net worth" can really weigh on someone, can't it? It's like looking at a measuring tape and realizing you're just not reaching the mark you had hoped for, or perhaps even the one you truly need for comfort and peace of mind.

When we talk about something being "too" a certain way, it often suggests it's beyond a suitable point, more than what's wanted or needed, but in this instance, it means more short than is comfortable. Think about the word "too" itself, as we often hear it used: it can mean something is in excess, or perhaps beyond a desirable level, as in "too much sugar." Here, with a net worth, it means it's excessively low, below a level that feels right or provides security. So, when your net worth feels "too short," it means it falls uncomfortably below what you believe is enough for your goals, for your plans, or for simply living with less worry. It's a feeling, really, that your financial foundation isn't as solid as you wish it were, a bit like having a very small piece of cake when you're quite hungry, you know?

This feeling, this idea of a net worth being "too short," is more than just a number on a spreadsheet; it’s about what that number means for your life, for your dreams, and for your ability to handle whatever comes next. It’s about feeling a bit behind, or perhaps like you're not making enough progress. But here's the good news: recognizing this feeling is the very first step toward making a real change. In this article, we'll explore what it means to have a net worth that feels "too short," why so many people experience this, and, crucially, some practical ways to begin building it up, starting today, this very year, in 2024.

Table of Contents

- What Does "Too Short Net Worth" Really Mean?

- Why Your Net Worth Might Feel "Too Short"

- Practical Steps to Boost Your Net Worth

- Changing Your Financial Mindset

- When to Seek Expert Help

- Frequently Asked Questions About Net Worth

- Conclusion

What Does "Too Short Net Worth" Really Mean?

When someone says their net worth is "too short," they're usually expressing a sense of dissatisfaction with their current financial standing. It’s not simply that the number is low, but that it feels inadequate for their present needs or future desires. This idea of "too" implies an amount that is more than what is suitable or enough in the negative sense, meaning it's more short than one would like. It’s about a gap between where you are and where you want to be, or where you feel you should be, in a very real way. This feeling can be quite personal, you know, and what feels "too short" for one person might feel just fine for another, which is interesting.

A net worth, in simple terms, is what you own minus what you owe. So, it's your assets (like savings, investments, property) less your liabilities (like loans, credit card balances, mortgages). When this number is "too short," it means that the value of what you possess isn't enough to cover your financial obligations or to provide the security you hope for. This can be a really unsettling realization, especially when you think about long-term goals like buying a home, paying for education, or, say, retiring comfortably. It’s a bit like trying to build a tall tower with not quite enough blocks, isn't it?

Beyond Just a Number

The feeling of a "too short net worth" goes beyond just the digits on a statement. It touches on feelings of security, opportunity, and freedom. For many, a low net worth can mean feeling stuck in a job they don't love, or perhaps unable to pursue a dream because the financial cushion simply isn't there. It can lead to worries about unexpected expenses, like a car breaking down or a sudden medical bill, which, you know, can happen to anyone. It’s about the peace of mind that a healthier financial picture can bring, and the lack of it when things feel a bit thin. In some respects, it’s about feeling a bit vulnerable to life’s curveballs, isn't that so?

- Bezos Store Discount Code

- French Prairie Gardens Oregon

- Calabar High School

- Dreams Usa

- Cyberkitty Onlyfans

This feeling is also tied to personal values and life stages. A young person just starting out might have a net worth that is technically low, or even negative due to student loans, but they have time on their side to grow it. Someone closer to retirement, however, might feel a "too short net worth" much more acutely, as their window for accumulating wealth is, well, rather smaller. So, it's about context, really, and what your current life situation demands from your finances. It's not just a universal benchmark, but a very individual one, you see.

The Feeling of "Too Much" or "Too Little"

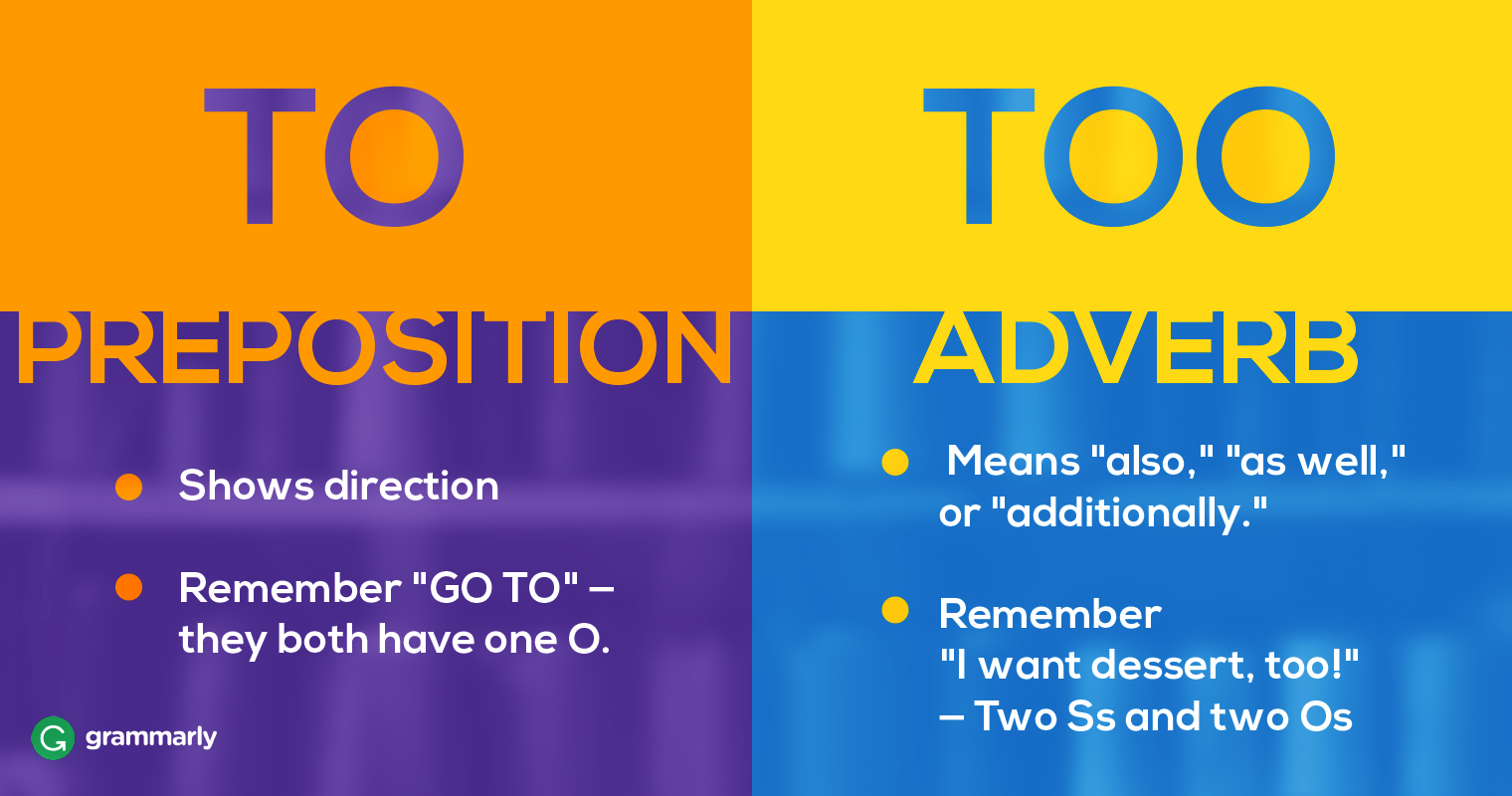

It's fascinating how our language uses the word "too." As "My text" points out, "too" often means "more than is needed or wanted" or "more than is suitable or enough." When we apply this to a "too short net worth," it means the *shortness* itself is beyond what's acceptable. It’s not just "short," it’s "too short" – an uncomfortable, undesirable level of financial insufficiency. This distinction is really important because it highlights the emotional weight behind the phrase. It’s a feeling of imbalance, like a scale tipped too far in one direction. You know, it's that sense of something being just a little off, isn't it?

This perception of "too short" can stem from comparing oneself to others, or to societal expectations, or even just to a personal ideal. Maybe you see friends buying homes or taking nice vacations, and you start to wonder why your own financial picture isn't allowing for those things. That can certainly make your own situation feel "too short." It’s a very human reaction, after all, to compare and contrast. But, as a matter of fact, everyone's path is different, and what's "too short" for one person might be just fine for another, as I was saying.

Why Your Net Worth Might Feel "Too Short"

There are many reasons why someone might feel their net worth is "too short," and often, it's a mix of different factors. Sometimes it's about the bigger picture, like what's happening in the economy, and sometimes it's more personal choices or circumstances. It's rarely just one single thing, is that right? Understanding these reasons can be a really helpful step toward figuring out what to do about it. It’s like trying to solve a puzzle; you need all the pieces to see the whole picture, you know.

One common reason is simply not earning enough to cover living expenses and still have money left over to save or invest. If most of your income goes straight out the door for bills, there's not much left to build up assets. This is a reality for a lot of people, especially with the cost of living seemingly always going up. It’s a tough spot to be in, and it can definitely make your net worth feel, well, rather short. And then there's the whole business of debt, which can eat away at any progress you make, can't it?

Common Financial Hurdles

One big hurdle is often student loan debt. Many people start their adult lives with a significant amount of money owed for their education, which can mean their net worth begins in the negative. It takes time, sometimes a lot of time, to pay that down and then start building positive assets. This is a pretty common story for younger generations, you know, and it definitely contributes to that feeling of a "too short net worth" early on. It's a bit like starting a race from behind the starting line, isn't it?

Another common issue is simply not saving enough, or not starting to save early enough. Life gets busy, and it's easy to put off saving for "later." But every year that passes without putting money aside means missing out on the potential for that money to grow over time, thanks to the magic of compounding. Also, unexpected expenses can derail even the best intentions. A medical emergency, a job loss, or a major home repair can quickly wipe out savings and push a net worth back down. These things happen, and they can feel incredibly unfair, honestly. They can definitely make you feel your net worth is "too short," or even make it shorter, so to speak.

Consumer debt, like credit card balances, is another significant factor. High-interest debt can feel like a heavy anchor, pulling down your net worth and making it very difficult to get ahead. The money you pay in interest isn't building your assets; it's just covering the cost of borrowing. This is a cycle that can be really tough to break, and it often contributes quite a bit to that feeling of financial struggle. It’s a bit like trying to run uphill with extra weight, you know, it just makes everything harder.

The Role of Expectations

Sometimes, the feeling of a "too short net worth" comes not just from the numbers themselves, but from our expectations. We might have an idea in our heads of what our net worth "should" be by a certain age, or what our peers seem to have. These expectations, whether realistic or not, can create a sense of disappointment if our reality doesn't quite match up. It's a very human thing to compare, isn't it? But, as a matter of fact, everyone's path is different, and life throws different challenges at us all, so comparing ourselves too much can be a bit unhelpful, can't it?

Media and social media can also play a part in shaping these expectations. We often see highlight reels of other people's lives, showing their successes and possessions, which can make our own situations feel less impressive. It's easy to forget that these portrayals often don't show the full picture, the struggles, or the debt that might be behind those shiny images. So, you know, it’s important to remember that what you see isn't always the whole story. It's like looking at a very polished photograph, you just don't see the messy bits around the edges, do you?

Practical Steps to Boost Your Net Worth

Feeling that your net worth is "too short" can be a powerful motivator for change. The good news is that there are many practical steps you can take, starting right now, to begin building it up. It doesn't have to be some huge, overwhelming task; often, it's a series of smaller, consistent actions that add up over time. It's a bit like building a wall, you know, one brick at a time. And every single brick, however small, makes a difference, so it's almost always worth getting started.

The key is to create a plan that feels achievable for you, given your unique circumstances. There’s no one-size-fits-all solution, but there are some general principles that tend to work well for most people. It's about making smart choices with your money, both in how you earn it and how you spend it. It's also about being patient, because growing your net worth is usually a marathon, not a sprint, as a matter of fact. But every step you take brings you closer to your goals, doesn't it?

Getting a Clear Picture

The very first step is to figure out exactly where you stand. This means calculating your current net worth. List all your assets: money in checking and savings accounts, investments (like retirement funds or brokerage accounts), the value of your home (if you own one), vehicles, and any other valuable possessions. Then, list all your liabilities: credit card debt, student loans, car loans, mortgages, and any other money you owe. Subtract your total liabilities from your total assets, and that's your net worth. You can find many helpful guides online, for example, this one from Investopedia, which explains how to calculate your net worth: How to Calculate Your Net Worth. This simple exercise can be quite eye-opening, you know, and it gives you a starting point.

Once you have that number, it’s a good idea to look at your income and expenses. Where is your money coming from, and where is it going? Creating a budget, or at least tracking your spending for a month or two, can reveal areas where you might be able to save more. Sometimes, we spend money without even realizing it, on small things that add up. Just seeing it all laid out can make a big difference, honestly. It’s like shining a light into a dark room; you see things you didn’t know were there, you know?

Strategies for Growing Assets

To increase your net worth, you generally need to do two things: increase your assets and decrease your liabilities. On the asset side, one of the most effective ways is to save and invest consistently. Even small, regular contributions can grow significantly over time, thanks to the power of compound interest. Think about setting up an automatic transfer from your checking account to a savings or investment account each payday. This way, you pay yourself first, before you have a chance to spend the money. This is a very simple, yet powerful habit, you know.

Consider exploring different types of investments, depending on your comfort level with risk and your time horizon. Retirement accounts, like a 401(k) through your job or an Individual Retirement Account (IRA), offer tax advantages and are designed for long-term growth. If you have an emergency fund already built up, which is basically a must-have, then putting money into these accounts can be a very smart move. Learn more about financial planning on our site, which can give you some good ideas. Diversifying your investments, meaning spreading your money across different types of assets, can also help manage risk, as a matter of fact.

Another way to boost assets is to increase your income. This could involve asking for a raise at your current job, taking on a side gig, or even learning new skills that make you more valuable in the job market. Every extra dollar you earn, especially if you can save or invest a portion of it, directly adds to your potential net worth. It’s about finding ways to bring in more money, you know, and there are often more opportunities out there than we initially think. Sometimes, just a little bit more can make a pretty big difference.

Tackling Debts Effectively

Reducing your liabilities is just as important as growing your assets. High-interest debt, like credit card debt, is often the biggest drag on net worth. Focusing on paying this down first can free up a lot of money that was going toward interest payments. Two popular strategies are the "debt snowball" and the "debt avalanche." With the snowball, you pay off your smallest debt first, which gives you a quick win and a psychological boost. With the avalanche, you pay off the debt with the highest interest rate first, which saves you the most money over time. Both methods work, it just depends on what motivates you most, you know.

Consider consolidating high-interest debts into a lower-interest loan if that's an option for you. This can make your monthly payments more manageable and reduce the total amount of interest you pay over time. It's like taking a whole bunch of small, expensive loans and turning them into one bigger, cheaper one. This can really simplify things, and save you money, which is always a good thing, isn't it? It’s about being smart with how you manage what you owe, which is just as important as how you manage what you own.

Also, try to avoid taking on new, unnecessary debt. Before making a large purchase, ask yourself if it’s truly needed and if you can afford it without going into debt. Living within your means, or even below your means, is a powerful way to ensure your liabilities don't grow faster than your assets. It’s a pretty simple idea, really, but sometimes it’s the simple ideas that are the hardest to stick to, you know? But, honestly, it makes a huge difference in the long run.

Changing Your Financial Mindset

Beyond the numbers and the strategies, a big part of improving a "too short net worth" involves shifting your thinking about money. Our attitudes and beliefs about money can have a huge impact on our financial actions. If you constantly feel deprived or overwhelmed, it can be hard to make consistent progress. It’s about cultivating a healthier relationship with your money, you know, one that feels empowering rather than disheartening. This is a very personal journey, and it takes time, but it’s definitely worth it, as a matter of fact.

It's about moving from a mindset of scarcity, where you feel there's never enough, to one of abundance, where you see possibilities for growth and security. This doesn't mean ignoring reality, but rather focusing on what you *can* control and the progress you *are* making, however small. It’s a bit like tending a garden; you focus on nurturing what’s there and planting new seeds, rather than just worrying about the weeds, isn't it?

Shifting Your Perspective

Instead of focusing on what you lack, try to appreciate what you have. Practicing gratitude, even for small financial wins, can help change your outlook. Did you pay off a small debt? That's a win! Did you save an extra $50 this month? Another win! These small victories build momentum and help you feel more in control. It's about celebrating the progress, not just waiting for the finish line, you know? Because, honestly, the journey itself is a big part of it.

Also, try to view money as a tool, a means to achieve your goals, rather than an end in itself. When you connect your financial actions to your dreams – whether it's travel, a comfortable retirement, or helping your family – it becomes much easier to stay motivated. It's not just about accumulating wealth; it's about what that wealth allows you to do and become. This kind of perspective can be really powerful, you see, and it can help you make choices that align with your deepest desires.

Small Steps, Big Changes

Remember that building net worth is a gradual process. You don't need to make drastic changes overnight. Even small, consistent steps can lead to significant improvements over time. For instance, saving just a little bit more each week, or finding one small expense to cut, can add up. It’s the consistency that truly matters, more or less. Think about it: if you save an extra $10 a week, that’s over $500 in a year, which is pretty good, isn't it?

Consider setting realistic, achievable financial goals. Instead of aiming to "become rich," perhaps aim to save a certain amount for an emergency fund, or to pay off one credit card. Once you hit those smaller goals, you can set new ones. This builds confidence and keeps you moving forward. You know, it's like climbing a mountain; you aim for the next ridge, not just the summit, and each ridge conquered makes the next step feel more possible. You can find more specific advice on savings strategies on our site, for example.

When to Seek Expert Help

Sometimes, despite your best efforts, the feeling of a "too short net worth" persists, or you might feel completely overwhelmed and unsure where to even begin. In these situations, seeking help from a financial professional can be incredibly beneficial. They can provide personalized advice, help you create a realistic plan, and offer guidance tailored to your specific situation. It’s like having a very knowledgeable guide for your financial journey, you know, someone who can point out the best paths and help you avoid pitfalls.

A financial advisor can help you assess your current financial health, set clear goals, and develop strategies for saving, investing, and managing debt. They can also help you understand complex financial products and make informed decisions. If you're feeling stuck, or if your situation feels particularly complicated, reaching out to someone with expertise can provide much-needed clarity and support. It's a bit like getting a second opinion from a doctor when you're not feeling well; sometimes, that professional insight is exactly what you need, isn't it?

There are different types of financial professionals, from financial planners who help with overall financial strategies, to debt counselors who specialize in helping people get out of debt. Do a little research to find someone who fits your needs and who operates with your best interests at heart. Look for certified professionals, and don't hesitate to ask about their fees and how they are compensated. Finding the right person can make a really big difference in your financial journey, you see, and it's an investment in your future well-being, arguably.

Frequently Asked Questions About Net Worth

Here are some common questions people often ask about their net worth, especially when they feel it's "too short."

What is considered a "short" net worth?

Well, the idea of a "short" net worth is actually quite personal and depends a lot on your age, income, where you live, and your financial goals. For a young person just starting out, a net worth that's even negative due to student loans is, you know, pretty common. For someone nearing retirement, a "short" net worth would mean not having enough saved to live comfortably without working. There isn't one universal number; it's more about whether your net worth feels sufficient for your current needs and

How to Use 'Too' and 'Enough' in English | Adverbs, English and English

To vs Too: What is the Difference Between To and Too - English Study Online

To vs. Too: How Should You Use To and Too? | Grammarly